What is Reverse charge Mechanism (RCM) under GST?

GST reverse charge mechanisms (RCM) means that the GST is to be paid and deposited with government by the recipient of goods /services and not by the supplier of Goods/services.

However, Under the RCM, the receiver of goods/services pay the GST to the supplier of goods/services and such supplier then deposit the GST with the Govt.

When is there Reverse charge Mechanism applicable?

- Supply from an Unregistered dealer to a Registered dealer(section 9(4)):-If a person not registered under GST, supplies goods or services to a person who is registered under GST, then in such cases RCM would get applicable i.e the GST would be required to be paid by the registered person directly to the Govt on behalf of the supplier. However, in case of supply of exempt goods/services, GST under RCM shall not be applicable.

- E-commerce operator will be liable for RCM. If the e-commerce operator absence in the taxable territory, then a person representing such electronic commerce operator for any purpose will be liable to pay tax. If the operator will appoint a representative who will be held liable to pay GST.

- RCM is also applicable on certain goods and services which are notified by the govt. reverse charge under section 9(3) is applicable for both inter-state as well as same state transaction .The goods and services on which GST shall be levied under the RCM.

Some List of goods/services under reverse charge mechanisms (RCM)

- Reverse charge on Goods under section 9(3)

| Nature of supply of goods | Supplier of goods | Recipient of supply |

| Supply of Cashew nuts, not shelled or peeled | Agriculturist | Any registered person

|

| Bidi wrappers leaves(tendu) | Agriculturist | Any registered person

|

| Tobacco leaves | Agriculturist | Any registered person

|

| Silk yam | Any person who manufactures silk yarn from raw worm cocoons for supply of silk yarn | Any registered person

|

| Supply of lottery tickets | State government, union Territory | Lottery distributor |

- Reverse charge on services under section 9(3)

| Nature of supply of services | Supplier of Service | Recipient of service |

| Any service supplied by any person who is in a non-taxable territory | Any person located in Non-taxable territory | Any person located in taxable territory other than non-taxable territory |

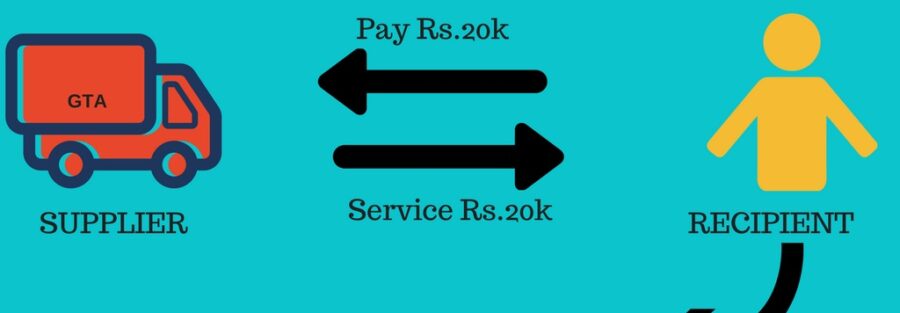

| Supply of services by a goods transport agency (GTA) who has not paid central tax at the rate of 6% in respect of transportation of goods by roads | Goods Transport Agency (GTA) | Any person registered under CGST, SGST and IGST Act

Anybody co-operates established, by or under any law

Any partnership firm if registered or not under any law

Any Casual person located in the taxable territory |

| Services provided by individual advocate by way of representational services before any court, tribunal, or authority by way legal services, to a Business Entity | Any individual Advocate including or firm of advocates | Any Business entity located in the taxable territory |

| Services provided by an Arbitral tribunal. | Any Arbitral tribunal | Any Business entity located in the taxable territory |

| Services provided by an insurance agent | An insurance agent | Any person carrying on the insurance Business. |