What is a Producer Company?

What is a Producer Company? In generic terms, producer companies can be said a legally recognized body of farmers/ agriculturists with the…

What is ROC filling and why we file the annual return of companies?

What is ROC filling and why we file the annual return of companies? Annual ROC Filing is filing certain forms to the…

Company Fresh Start Scheme 2020

As the whole world is fighting against pandemic Covid19, and as in last few years Ministry has received requests from various stakeholder…

03

Oct 22

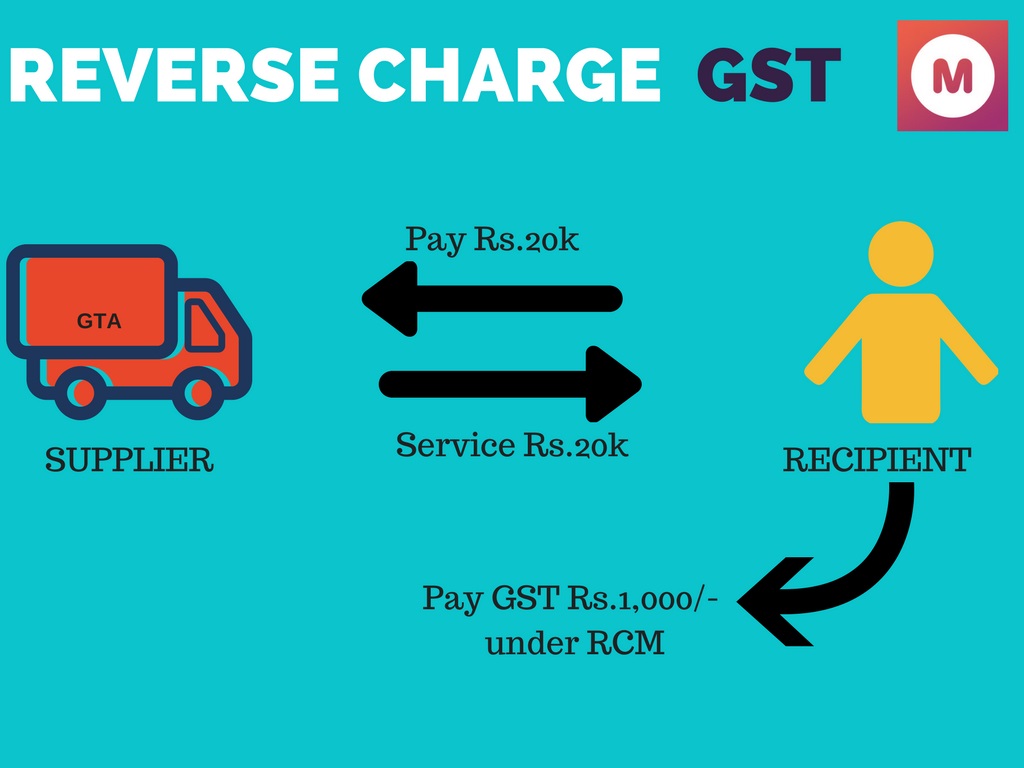

What are the goods and services which comes under Reverse charge mechanism(RCM)?

What is Reverse charge Mechanism (RCM) under GST? GST reverse charge mechanisms (RCM) means that the GST is to be paid and…

03

Oct 22

Income Tax Assessment

Income Tax Assessment Every year all the citizens in India are expected to submit their income tax return furnishing their income details,…

Certificate of Business Commencement FORM INC-20A

In Companies (Incorporation) Fourth amendment 2018 MCA has re-mandated that every company registered after 02-11-2018 has to file a declaration in the Form-20A along…